Employee Stock Purchase Plans (ESPPs) are one of the most powerful savings tools out there and not enough people are using theirs! In fact, Deloitte did a study on this and found 37% reported a participation rate of less than 25% by their eligible employees. And nearly 32% report a participation rate between 25 and 50%.

Why are people not using their ESPP plans? My thought, it’s simply because most people do not understand how beneficial they are when you leverage them correctly.

In this blog post I am going to walk you through:

Let’s get right into it!

An ESPP plan is a way for your company to incentivize you/reward you through their stock vs cash bonuses. But know that many companies actually offer both to their employees.

With an ESPP plan you are able to opt-in to the program and buy your employer stock at a certain cadence. There is typically an enrollment period where you get to choose if you want to use this benefit and at what percentage or your income you want to use for it. You typically are allowed to buy up to $25,000 a year through the ESPP plan.

Over the next 6 months, that percentage of your income (or dollar amount you pick) is withheld to purchase said stock at the end of the period called the purchase date. Some plans do quarterly or annually, but the most common by far is semi-annually.

At the end of the purchase date, your company will buy that dollars worth of stock. Here’s an example to help illustrate it.

You elected to do $25,000 a year. So over the next 6 months your employer withholds $12,500 to be used at the purchase date to buy your company stock. The price is $100 a share at the purchase date so the company buys you 125 shares.

However, most the time there is a benefit where you get some sort of discount. This could be anywhere from 5-15%. I have also seen plans where for every 3 shares you buy they give you a 4th. All of these discounts are really helpful as you get to buy more for less dollars.

So using the example above, if you got a 15% discount, on the purchase date the price of the shares to you would be $85. This means you would be able to get 147 shares due to this discount. This is way more than the example above. I hope you are starting to see how powerful this can be!

Now let me throw another benefit some offer called a lookback provision. This means that you will get the lower price of either what it is at the beginning of the offering period or at the purchase date. Let’s look at another example.

Let’s say the price of the stock is $90 at the beginning, then it ends at $100. With the lookback provision, you would be able to buy the shares at 15% off of $90 = $76.5. So your $12,500 would now buy you 163 shares!

The combination of the lookback provision and discount can be so powerful.

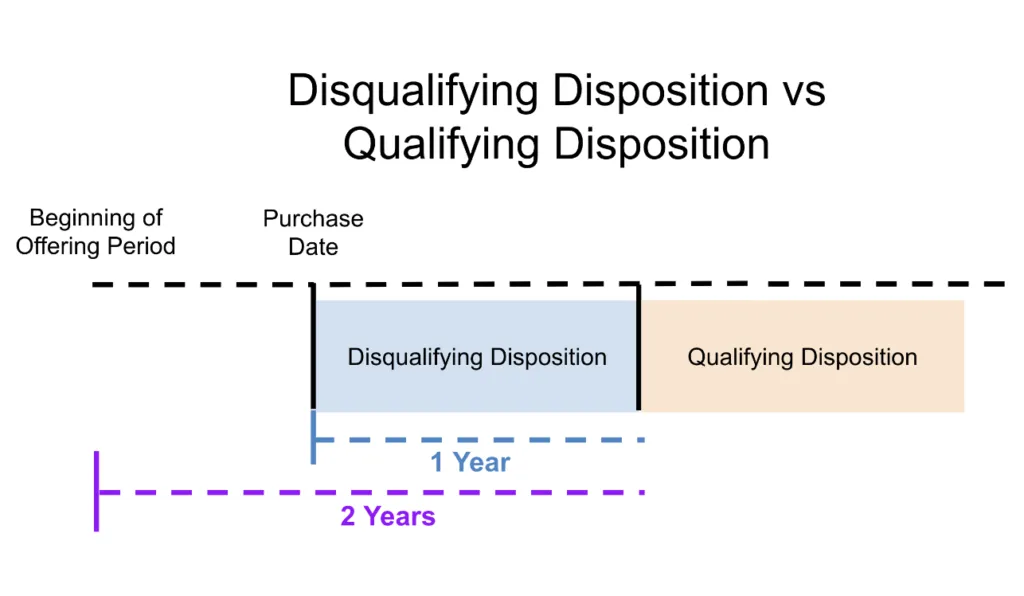

ESPP plans tax impact comes when you choose to sell the shares. And when you sell the shares determines whether you pay short term capital gains or long term capital gains rates. These are referred to as a qualifying position or disqualifying position. Let’s walk through each.

To get long term capital gains you have to meet two requirements:

However, note that the discount you received is still taxed as ordinary income no matter how short or long you hold the shares for.

In the example above, when we got to buy for $85 when the share price was $100, the $15 discount is taxed at short term capitals gains rates. Then if you meet the qualifications above and sell for $120 later on, the $20 will be taxed as long term capital gains which comes at more favorable rate.

A disqualifying position happens when you do not meet both the requirements above. So if you sell before those dates are met, it will all be taxed at your income rate. Using the same example, let’s say to sell a couple months after you are able to for $105. The $15 discount + the $5 gain is all taxed as short term capital gains.

This picture should help show you the difference between the two:

Many do not understand this, but if you have a 15% discount, you immediately are getting a 17.6% rate of return. Here’s the math on it to. If the price on the purchase date is $100, then you get to buy for $85. This means your $85 bought $100 worth of shares. The growth rate = ($100 – $85)/ $85 = 17.65%.

There are not many other ways to be able to get that return without a ton of added risk. We work with many families who know they want to maximize this, their HSA, 401k, dependent care FSA, etc. which puts them at a negative cash flow position monthly. We then use the ESPP proceeds to supplement this and replenish their emergency fund.

This is how you create efficiencies with your hard earned money!

There is no right answer here on how you should sell them. Each person and situation is different. However, I will say that many see the information above and think they will choose to just wait for long term capital gains to sell. But… understand you are running the risk that the stock does drop over the period of time. I typically prefer choosing to sell right away and lock in the gain if you plan to not hold the position.

If you want to get more exposure to your company, then holding could make sense.

I hope this better helps you understand ESPP plans, how they work, how they are taxed, etc.

Thanks for reading!

If you need help maximizing your employer stock, feel free to head on over to allstreetwealth.com and apply to work with us.

Disclaimer: none of this should be seen as advice. This is all for educational purposes.

Financial Advisor